How the Economic Machine Works, How it Grows and Why it Crashes

Hi!

It’s Vincent. Since I’ve been working from home, I’ve had a lot more time to write again. Given the current situation, I thought a good topic for me to add value to everyone is around how the economy works - from the first principle 😊. I hope you like it!

Understanding the economy isn’t just for governments, financial institutions, and bankers.

It affects all of us.

In fact, the majority of the money in the economy is made up of everyday people’s pensions. That is OUR money, OUR future, OUR retirement dream of owning a farm with our partners, families, maybe a few SUPER CUTE Aussie Shepherds.

During the 1930 – 1932 market crash, $1 dollar in your pension/investment fund, after 2 years, suddenly is only worth $0.13 dollars ($12.9 cents) [source: Fed Reserve Bank St. Louis]. In other words, if you’ve worked your butt off for 40 years to save up $1,000,000, it’s value would have shrunk to a mere $129,000 in just 2 years. Worst of all, it stayed that way for the next 20 years…

Most of us know something is happening with our economy, our jobs, our future. But we don’t know what to do until it is too late…

As I’m going through my first financial crash as an [educated] adult, I thought the best way for me to contribute to the world right now is to share my studies and thoughts on what is happening, why it’s happening and what we can do to come out better on top.

While the spark of this crisis is due to the COVID-19 global pandemic, the real reason for the crash is because of something else. To best illustrate this, I’ll condense things down into first principles and sketches.

I wish this is something I’d studied as a kid going through school. Special thanks for Adam Smith, Ray Dalio, Warren Buffet, Charlie Munger, Peter Schiff, and Naval Ravikant who have taught me so much by writing and sharing their wisdom.

The island in the story I’m about to tell is inspired by my love for… Bali.

How Wealth is Created Through Innovation

May 7, 2020

Story

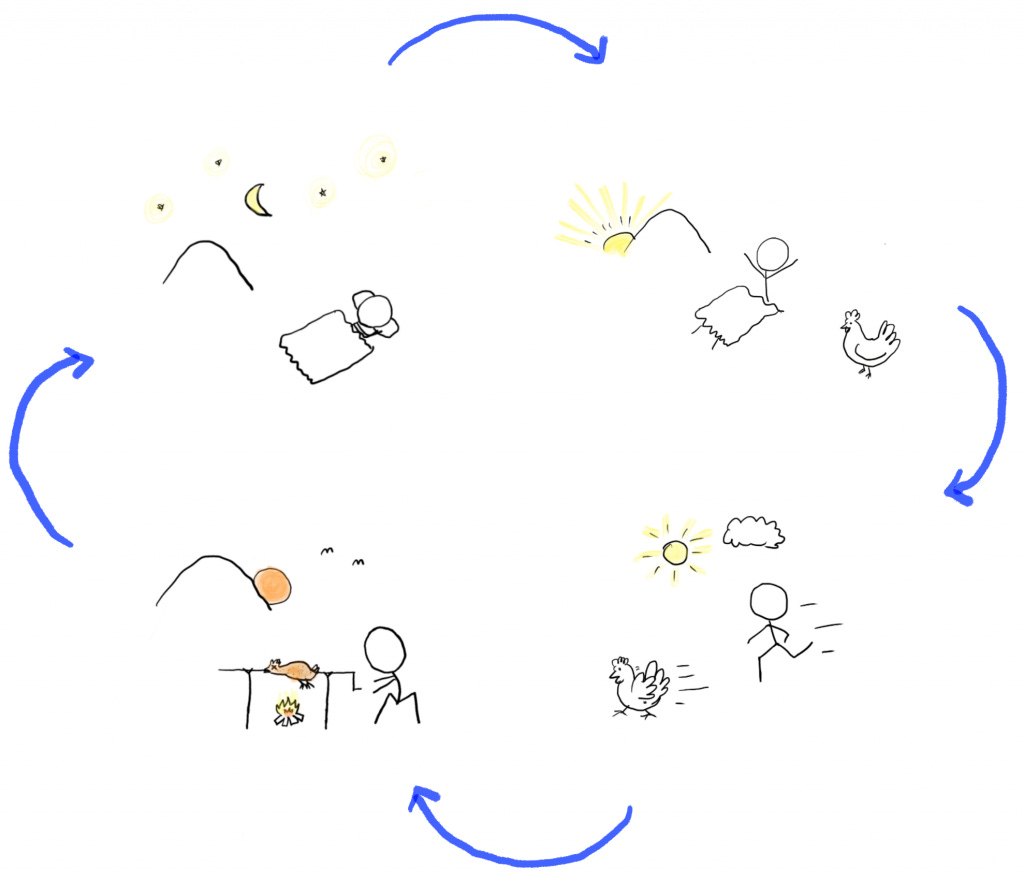

Once upon a time, there were three people – Amy, Benny, and Charlie – who lived on an island alone. The island was a rough place with no luxuries. Food options were extremely limited. The menu consisted of just one item: chicken.

The island was surrounded by an abundance of a strangely homogenous population of chickens. Any one of these chickens was large enough to feed one human being for one day.

However, this was an isolated island where no human technology was yet available. So the best way for everyone to eat is to chase and catch a chicken every day by hand.

Using this inefficient technique, each person was able to catch one chicken per day, which was just enough for them to survive to the next day. This activity amounted to the sum total of their island economy. Wake, hunt, eat and sleep.

This is a super simple, chicken-based economy where there’s

No savings

No credits

No investments

Everything that is produced is consumed.

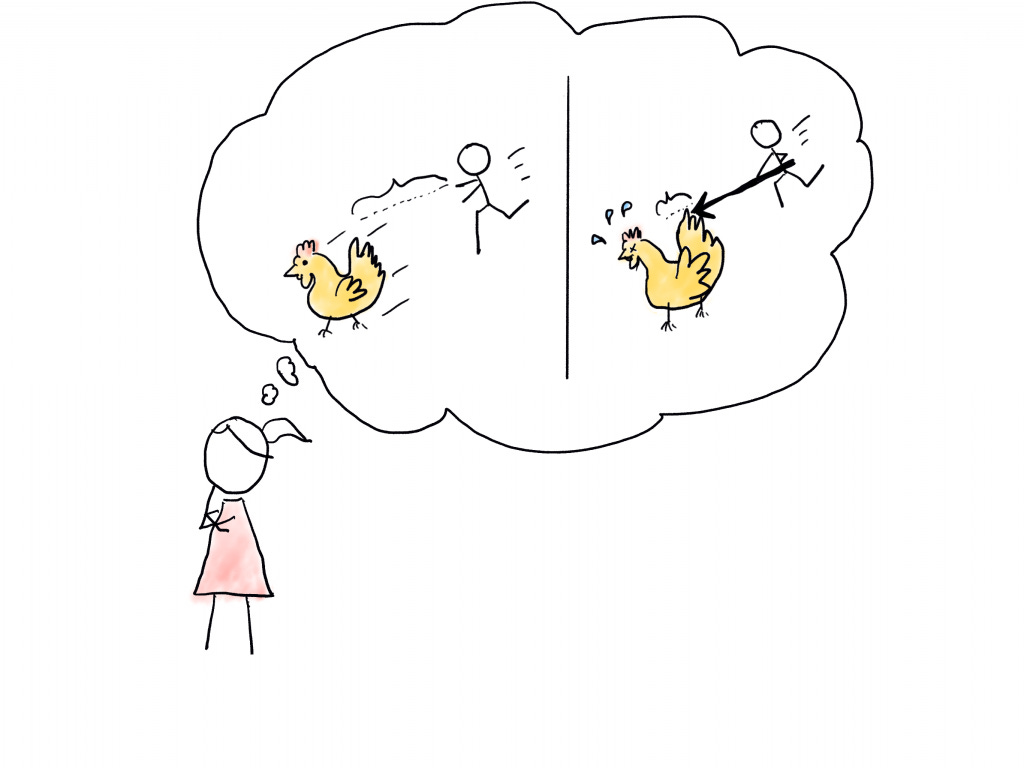

In order to improve their lives beyond their subsistence level, the island tribe realise they need to catch more than one chicken a day.

One night, Amy ponders the meaning of life, asking: “Is this all there is?” Suddenly an idea formed in her head – she needed a device that vastly increases her reach to catch a chicken. She set out to find the materials to build one. She decided to call this device a “spear”.

The next day, Benny and Charlie realised Amy wasn’t focused on hunting. After asking Amy about her idea of building a spear to “revolutionise the way they catch chicken”, they both rolled their eyes and thought their friend had lost her mind…

Determined Amy keeps on sharpening a long piece of wooden stick.

By the end of the day, Amy has created her spear. She has created capital by taking on risk, underconsumption, and making sacrifice.

That night, while Benny and Charlie slept with full stomachs, Amy dealt with hunger pangs and physical exhaustion. Still, she’s hopeful that she’s done the right thing and is motivated by a bright, chicken-filled future.

………

The next day, Benny and Charlie made fun of Amy’s invention. Undeterred, Amy charged into a nearby garden. Ridicule kept coming as she awkwardly handled her strange new device.

After a few minutes, she got the hang of it and caught her first chicken. Benny and Charlie stopped laughing. Amy landed her second chicken within her next hour of hunting. the boys were in awe. After all, it generally took them all day to get just one chicken!

From this innovation, the island’s economy was about to drastically change. Amy had just increased her productivity, and that was a good thing for everybody.

Amy pondered her sudden boon. “Since I can provide two days of food with only one day of hunting, I can use every other day to do something else. The possibilities are endless!”

First Principles

Underconsumption

In order to build her spear, Amy is unable to hunt for that day. She has to forgo the income (one chicken) that she would have otherwise caught and eaten. It’s not that Amy lacks the demand for chicken. In fact, she loves chicken and she will go hungry if she doesn’t get one that day. But she is choosing to defer that consumption in order to potentially consume more in the future.

Risk-Taking

Amy is also taking a risk because she has no guarantee if her idea of a spear will work, or allow her to catch enough additional chickens to compensate for her sacrifice. If she had failed, she would have starved and would expect no compensation from Benny and Charlie.

Capital

In economics, capital is a piece of machine that is built and used not for its own sake, but for building or making something else. Amy doesn’t want the spear, she wants the extra chickens the spear brings. Therefore, the spear is a piece of capital. It’s a machine that allows her to catch more chicken per day.

It’s valuable.

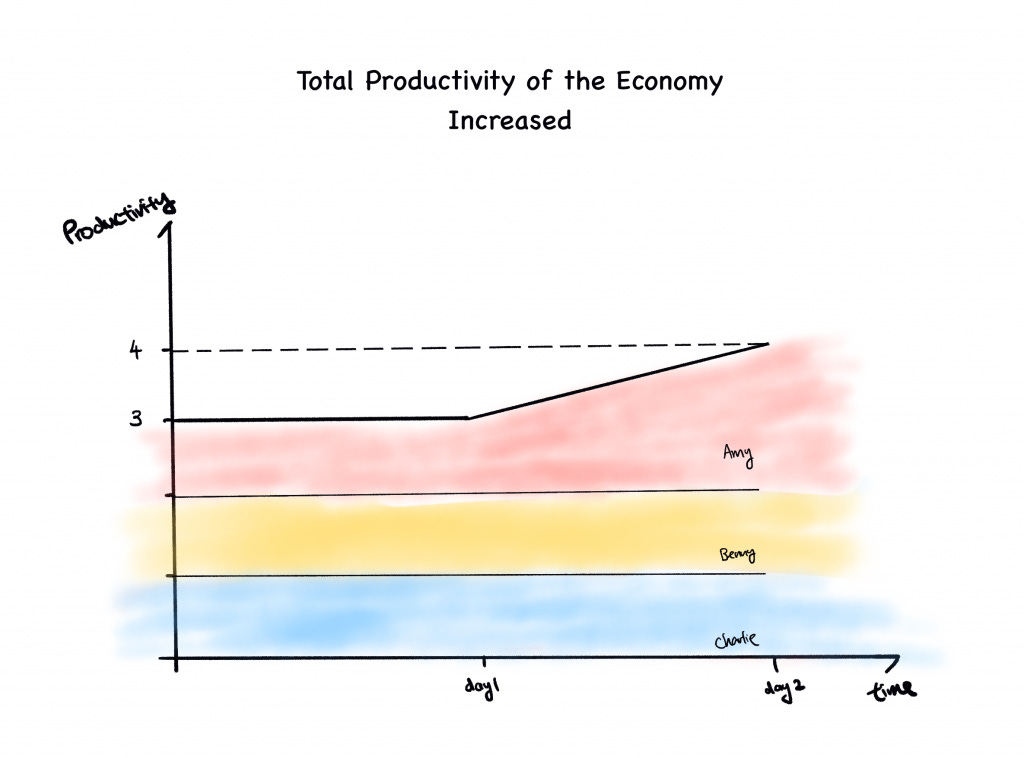

Productivity is King

The simplest definition of economics is the effort to maximize the availability of limited resources to meet as many human demands as possible. Just about every resource is limited. Tools, capital, and innovation are the keys to this equation.

By doubling her productivity, Amy is now able to produce more than she needs to consume. From her gain in productivity, the benefit will flow to all others in the economy. Her willingness to take a chance and go hungry led to the island’s first piece of capital equipment, which produces savings (for this story, let’s assume her chickens do not spoil). This saving is the lifeblood of the economy – not consumption.

Keeping this in mind, it is easy to see what makes economies grow: finding better ways of producing more stuff that humans want. This doesn’t change…no matter how big an economy eventually gets.

Do you like this chapter? There are more coming!

Subscribe to get the next update every two weeks and share it with your friend. It means the world to me.

Thanks! ☺️